© 2026 Trade Properties, LLC. All Rights Reserved. Privacy Policy. Terms of Use. Sitemap. Real Estate Website Design by Agent Image

Main Content

1031 Exchanges

A 1031 exchange (also known as a like-kind exchange) allows real estate investors to defer capital gains taxes on the sale of an investment property by reinvesting the proceeds into one or more replacement properties of equal or greater value. Under IRC Section 1031, this applies only to real property held for productive use in a trade or business or for investment.

1031 Exchanges

Keys to Success

1031 exchanges can be challenging projects. The relatively short window for identification of the upleg asset(s) combined with the complexity and unknown factors entering a real estate transaction present transaction risk and can blur investment objectives. Have a plan, know the market, and make sure you have the right partners to get the job done.

1031 Exchanges

Requirements

Like-Kind Property

Qualified Intermediary

Strict Timelines

Equal or Greater Value and Full Reinvestment

Investment Intent and Holding Period

Proper Reporting

1031 Exchanges

Requirements

Both the relinquished (sold, downleg) and replacement properties (upleg) must be real estate in the U.S. Most investment real estate qualifies (e.g., rental properties, land, commercial buildings), as long as it's not considered personal property.

1031 Exchanges

Requirements

A neutral third-party QI is required for delayed exchanges (the most common type). The QI holds the sale proceeds to avoid "constructive receipt" by the seller, which would disqualify the exchange. You cannot use a relative, agent, or attorney.

1031 Exchanges

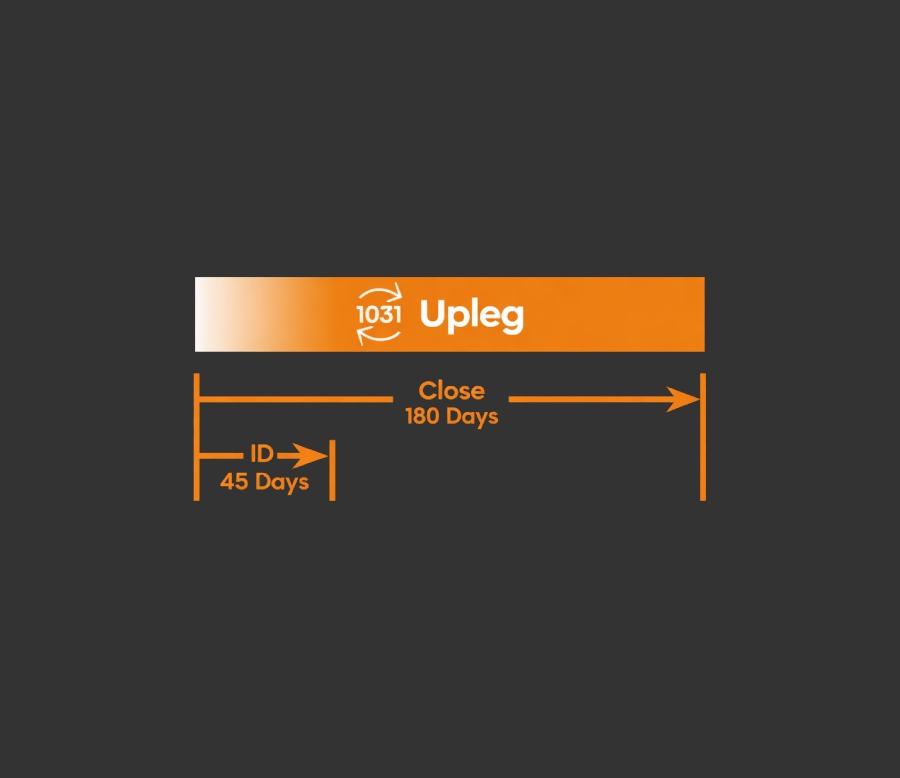

Requirements

- 45-Day Identification Period — Identify potential replacement properties in writing within 45 calendar days of closing the sale of the relinquished property. Rules include the Three-Property Rule (up to three properties) or the 200% Rule (any number of properties if total value ≤ 200% of relinquished property).

- 180-Day Closing Period — Close on the replacement property within 180 calendar days of the relinquished property sale (or tax return due date, whichever is earlier).

1031 Exchanges

Requirements

To fully defer the tax from the relinquished property, the replacement property must have a fair market value greater than or equal to the relinquished property, net of closing costs. All net proceeds must be reinvested. Any cash or debt relief received ("boot") triggers proportional taxable gain.

1031 Exchanges

Requirements

Both properties must be held for investment or business use. While there's no strict minimum holding period, the IRS often scrutinizes short holds; 1–2 years per property is recommended to demonstrate intent. Consult a tax professional.

1031 Exchanges

Requirements

The IRS requires special reporting on your tax return for the year of the exchange. Consult a tax professional and experienced QI early, as rules are strict—failure disqualifies the deferral entirely. For official details, see IRS resources on like-kind exchanges.

BACK TO SERVICES